In early May Anthropic announced it intends to be the infrastructure layer underneath the legal market. Not a tool or a vendor, the plumbing. Harvey, Thomson Reuters, iManage, LexisNexis — all pivoting to integrating rather than competing. A simplification, for users perhaps. Though when the plumbing is universal, so is the water pressure; if every party to a negotiation is running the same probabilistic analysis on broadly the same data, the answers start to look kind of the same too — worth asking what we’re simplifying toward.

That phrase, “broadly the same data”, is worth pausing on. Most legal AI systems sit on top of the same foundation models, trained on broadly the same underlying corpus. Firms then layer on proprietary context: retrieval-augmented generation (RAG) connected to firm repositories, matter histories, playbooks, practice guidance, practice questionnaires, and ultimately the individual prompt. Those layers matter, but they are also progressively smaller, by orders of magnitude. Trillions of tokens sit at the foundation. Thousands of documents sit in the firm repository. Hundreds of words sit in the practice questionnaire. Tens of words sit in the prompt. The contextual layers can meaningfully shape the output, but they do not replace the common foundation beneath it. That is what “broadly the same data” means in practice.

For the companies that have been building — and raising money — at the application layer, the announcement raises a question which has been surfaced with increasing frequency over the last four weeks, and which they’d probably rather not answer publicly: what, and how deep, is their moat now? The reaction has been either exhilarating or alarming. Both responses share an assumption worth examining. They assume we know what AI is replacing. We don’t.

Every productivity claim in legal AI rests on a number that, where it has been measured, has not been shared — at least not in a form that answers the question. Legal spend platforms have analyzed what gets billed — already value-adjusted by the partner before it left the building. Costs assessment proceedings occasionally surface what was recorded. Neither tells you what was actually done, or for how long.

The vendors can tell you the saving. Harvey can tell you a lawyer saves fifteen to thirty minutes per query1. Clio’s annual Legal Trends Report (the most rigorous public attempt to measure how lawyers actually spend their time, though focused on small to mid-sized firms) tells you that the average lawyer bills just 2.9 hours of an 8-hour day. Those numbers are at least testable.

And those are just the drafting and research use cases. Add M&A due diligence, compliance mapping, matter intake, document production — the list of applications is genuine and growing. The saving, across all of them, has almost certainly been measured. Internally. By the vendors, by the firms, by the platforms sitting on top of the billing data (though of course billing data represents only that which the partner believed the client would see value in, not what was done).

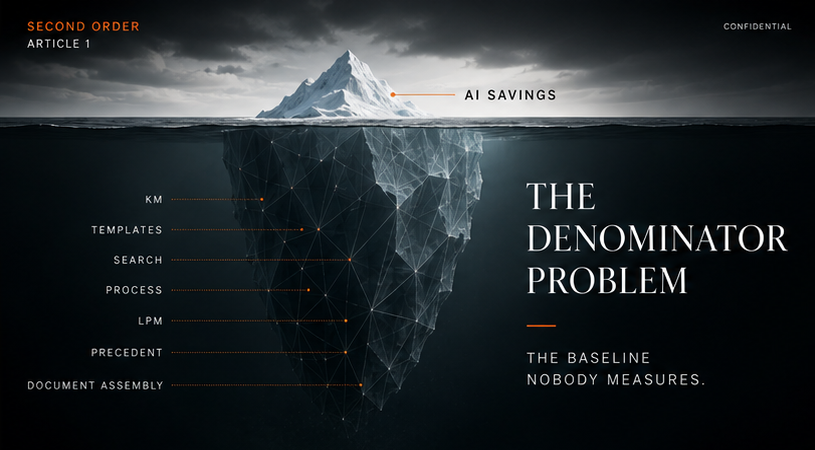

The denominator — what proportion of a lawyer’s day, just how many hours those tasks represented before the tool arrived — is not publicly known. And the people who do know have no incentive to say.

It would be a brave firm to publish the numbers; to say “we used to spend 100 hours on pre-acquisition due diligence per $10 million of transaction value and now we do it in ten” is to simultaneously hand your clients a fee reduction argument, your competitors a positioning opportunity, and the market a benchmark nobody asked for.

This matters more than it might appear. Because the investment case for legal AI at current valuations doesn’t just require the saving to be real. It requires the baseline to be large enough that the saving is commercially significant, and it requires the saving to survive the cost of the tokens that produce it. Those economics are moving awkwardly. The price of a given level of AI capability is falling fast, but the newest models consume far more tokens to reach it, and the subsidies that masked the true cost are being withdrawn, plan by plan and limit by limit. Cheaper tokens, more expensive work. And the implicit baseline in most of these conversations still looks a lot like 1990. Even if not explicitly stated, the rhetoric around AI suggests (perhaps deliberately?) that without it lawyers are drafting, negotiating, researching from blank sheets of paper and statute books.

What that rhetoric minimizes is the impact of the preceding waves, of the last 36 years of incremental change: Knowledge management systems compressed research and retrieval time. Document assembly tools compressed first-draft time. Clause libraries and template platforms compressed standard drafting time. Westlaw Edge compressed legal research time. Predictive coding compressed document review time. Process maps, playbooks, LPM — while none remain keynote topics today, they left a mark on the sand. Each wave took a bite out of the denominator. Nobody measured the bites. The compression happened incrementally, invisibly, absorbed into working practice without anyone systematically recording the before and after.

By the time Harvey launched in 2022, a transactional associate at a well-run firm was already starting from a heavily annotated template, pulling pre-negotiated clause variants, working from a KM system with vetted precedents. To suppose that associates at a serious firm are still drafting from a blank page is to misunderstand what the last thirty years of legal technology actually did. The blank page that anchors most AI productivity narratives had already largely disappeared. Or that was at least true in the practice areas amenable to those approaches. One question worth exploring is whether this wave of AI is any more applicable to the niche practice area — to the ten-person practice group whose drafting style is meaningfully and necessarily different from the broader firm corpus — than the previous approaches were. Practice Group questionnaires are a step in recognizing this limitation.

None of this means AI doesn’t help. It does. The floor has risen dramatically — a solo practitioner or under-resourced firm can now draft or research at a level that previously required institutional infrastructure. That democratization is real and genuinely valuable.

But the marginal productivity gain for the firms whose economics the market is watching is almost certainly smaller than the valuations imply. Because those firms have been compressing that denominator, quietly and continuously, for thirty years.

There is a version of this observation that has been true since Lexis launched in 1973. Rates at the top of the legal market have risen through every technology wave. Lawyer headcount has grown through every technology wave. The productivity dividend has been captured as margin, not passed to clients. The people predicting structural transformation of the profession have been predicting it, with each new technology, for fifty years.

The most durable career in legal is not partner. It’s prophet. The predictions don’t have to come true. They just have to be interesting enough to keynote again next year.

There is a valid counterargument: law firms are investing in these tools — Harvey’s first major law firm partnership was with A&O — which suggests they believe the productivity case. But investment and belief in the productivity case are not necessarily the same thing. Firms invested in extranets in 1999. Clients asked about them in RFPs, firms answered yes, vendors made money, and almost no one used them in practice. The investment was real. The productivity gain was not the point. When AI capability appears in every client RFP, every lateral recruitment conversation, every press ranking of innovative firms — the signal has value regardless of what the denominator turns out to be. Buying the signal is rational. It just isn’t the same as proving the case. Which is why the most revealing move in the market is the one that refuses to buy the signal at all. In late May 2026, Kirkland & Ellis, the highest-grossing firm in the world, said it would spend $500 million building its own AI platform on top of the same frontier models its rivals can also license, and would let no competitor license what it builds. Its chairman’s reasoning was that off-the-shelf tools are “raising the floor for everyone, but we don’t get hired for the floor.” A floor that everyone shares is not an advantage. The foundation is common to everyone. What Kirkland is paying half a billion dollars for is the layer on top of it, the one thing the shared model cannot supply: its own judgment, encoded, that no rival can also claim. Buying the signal is rational. Building past it is the tell that the signal has stopped meaning anything.

This isn’t an argument that nothing changes. Things change. The question worth sitting with — the one nobody seems to be asking in the weeks since Anthropic’s announcement — is: change relative to what baseline, captured by whom, and measured how?

If you’re responsible for legal spend, ask yourself a simple question: what percentage of the work you are paying for today is actually being compressed by AI, rather than by the thirty years of technology that came before it? If you don’t know the answer, how will you recognize the difference between a genuine productivity gain and a productivity gain that has been counted twice?

The saving is known (or knowable). The baseline isn’t. And without the baseline, the saving is just a number looking for a denominator. The people who know what that denominator looks like today — not what gets billed, but what gets done — aren’t saying. They have no incentive to.

That’s where the conversation should start.